Interview to Aniceto Saragossa, general director of Oficemen

Like key element in the public work and in the construction, know the evolution that comes following the production and the consumption of cement in our country during the last years can draw us a very approximated portrait of the situation that crosses this sector. For this, in Interempresas, have had the opportunity to interview to Aniceto Saragossa, general director of

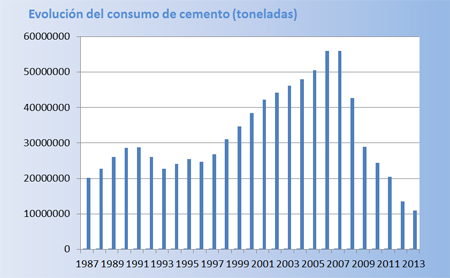

According to the last data that have contributed from Oficemen, the consumption of cement in Spain closed the 2013 with a fall of 19%. It considers that already it has hit rock bottom ?

Lamentably, no. After the fall in 2013, that has situated the total consumption of cement underneath of the 11 million tonnes, the forecasts for 2014 are not more alentadoras. The figures esperables of public investment and the paralización in that it follows immersed the real-estate sector endorse a new fall that will oscillate between a 7 and 8%. If our forecasts are hit, the domestic market would close the year 2014 in some 10 million tonnes.

For the moment, the consumption of cement in Spain has fallen again in January 13,6%. The year has initiated therefore, without indications of recovery in the sector and with a percentage of worse fall to the planned, since it duplicates to the expected for the group of the year by Oficemen.

It supposes this 19% the greater fall from the start of the crisis? Which is the descent accumulated so much in production as in consumption of cement in Spain?

From the start of the crisis have gone sucediendo consecutive falls of two digits until accumulating a total descent, in the last six years, of 80%. The greater fall porcentual produced to the closing of 2012, with 34%, what supposed in his moment the greater descent porcentual suffered by the domestic market Spanish in his recent history. It would be necessary to trace back to 1936 to find a greater fall.

In absolute terms, the domestic market Spanish has happened to consume almost 56 million tonnes in 2007, to less than 11 in 2013.

How reflects this collapse in losses of places of work and in business mass?

Whereas the domestic market has fallen around 80%, the employment only has done it 43% in the same period. So alone two factories have closed from the start of the crisis. The industry cementera has characterised always for being a sector with stable and qualified employment, in which employers and unions keep a narrow collaboration aunando efforts, always with the aim to reach a sectorial stability.

Nevertheless, the sector is going through moments of adjust hard, since as it mediates the rooted factories in our country only are working to 40% of his installed productive capacity.

There is some precedent in the history of our country in which it finished the year with a consumption of inferior cement to the 11 million tonnes?

The figures of current annual consumption are similar to which had our country around the middle of the decade of the years sixty of the past century. Nevertheless, the indicator macroeconómico more reliable to establish a comparative is the data of per capita consumption, that allows to compare the figures taking into account the volume of population that consumes the cement. In this context, the per capita consumption more similar to the reached in 2013 is the one of the year 1962, that rondaba the 220 kg/hab.

After this strong fall of the market, in which levels moves Spain with regard to other European countries?

Basing us in the per capita consumption, only United Kingdom (153 kg/hab/year), Greece (221 kg/hab/year) and Holland (263 kg/hab/year) had an inferior per capita consumption to the of Spain in 2012 (according to the last available data for the total EU-27).

Of the current production of cement in Spain, which percentage allocates to the export?

In 2013, Spain exported 6,7 million tonnes, 8% more than in 2012, what supposes almost 40% of the cement produced in our country. In the actuality, Spain is the first exporter of cement of the EU, representing 18% of the community total exports and almost 26% of the no community.

Which has been the evolution of this distribution (national/export) from the start of the crisis?

In the years of greater economic bonanza, around the middle of the decade of 2000, Spain arrived to be the first consumer of cement of the EU, with a quota of 22,6% on the European total and with some levels of per capita consumption of 1.278 kg/inhabitant. Like this, and even having all the factories working to 100% of his installed capacity, the sector resorted to the imports like consequence of the impossibility to absorb the big demand confined of the Spanish market. Spain situated then , in the year 2006, in command of the importing of cement to European level.

Which are the main fortresses of our cement in the international market?

And the main barriers for his export?

Unfortunately, in the last years, the energetic cost in general and the electrical in particular have elevated the costs of production with regard to the ones of other countries of the surroundings, subtracting competitiveness and ralentizando the sales in the international markets.

In concrete, how affects to the sector these vaivenes that are producing in our country in matter of energetic politics?

As it said, the encarecimiento imparable of the electrical final cost in Spain has been the main escollo to increase the exports. It is a very mature market and competitive, where any swing in the costs can cause the immediate loss of a market, from here the ralentización of last months.

The industrial consumers electro-intensive, as it is the case of the Spanish industry of the cement, need a final price of the competitive electrical power in front of which have his competitors in other countries of his surroundings and, especially, more stable, what would allow to contemplate them in the half and long term.

Of face to the future, which forecasts have from Oficemen for the next years?

More difficult results still know when will be able to speak really of recovery, a concept conditioned to the return of the levels of own consumption of a country industrialised like Spain, that, given the volume of population and the surface, would have to rondar the 20 or 25 million annual tonnes.

And inside the general frame, in which sector have put greater expectations of recovery: edificación residential, no residential or civil public/work?

The first step so that it can recover any one of these subsectores is that it go back to flow the credit, what to his time would activate other variables like the employment, the consumption and the house. All this redundaría, finally, in a recovery of the public investment.

Now that speaks of the public investment, the true is that in the last years, the endowment of the General Budgets of the State for the investment in infrastructures has not stopped to go down (-8,6% in 2014, -13,5% in 2013, -28,1% in 2012 and -35,1% in 2011). It can allow really Spain this tendency?

From Oficemen do not tire us to repeat that, to continue with this tendency, our infrastructures will lose the train of our European neighbours and with them, the group of the industry. The Program of Stability of the Realm of Spain for the period 2013-2016 prolongs the restriction of the public investment, estimating a half volume of annual bidding from among 4.000 and 5.000 M, a fifth part of the volume licitado in the year 2010. This plan has situated the public investment in his lower historical volume and will separate us definitively of our European partners that in the next years will follow increasing the investment to good rhythm.

By all what Unit has signalled in this interview, seems evident that can not have recovery in Spain without taking into account to the construction. It is not like this?

Sure enough. Although in the years of crisis has extended between the public opinion, the belief that in Spain has built in excess and no longer remains at all for doing, this affirmation, no by repeated, has become true. The true is that the public investment Spaniard in the two last decades is far from to be abnormal since it situated in similar values in relation to the GDP to the ones of Luxembourg, Holland, France or Sweden. What himself could describe as abnormal is the situation lived from 2009, that has situated the public investment in the historical minimum of the statistical base (from 1964) with 1,3% of the GDP.

It is not unfair to blame to this sector of the big evils of the country?

In our country airports without aeroplanes to the margin- there is a good number of infrastructures that are far of the best European practices. They are the discreet infrastructures' between which can include the elimination of the necks of bottle in the accesses to the big cities, the suppressesion of ancient outlines in our roads, the rail connections with Europe, the networks of saneamiento and stations of purification of small and average populations, the hydraulics supply of arid zones of Spain, the improvements in the logistical networks all they indispensable for the correct economic development and industrial of any country.

")